Ownership

Valuation

Exploring the impact of Federal Reserve actions on interest rates and the future outlook for consumers, borrowers, and investors.

The Federal Reserve plays a crucial role in setting interest rates in the United States. As the country's central banking system, the Federal Reserve has the power to influence short-term interest rates through its monetary policy decisions.

One of the key tools the Federal Reserve uses to control interest rates is the federal funds rate. This is the interest rate at which depository institutions lend reserve balances to each other overnight. By adjusting the federal funds rate, the Federal Reserve can stimulate or slow down economic activity and attempt to control inflation.

The Federal Reserve actions and forward guidance have a large impact on interest rates that consumers pay and stock market expectations.

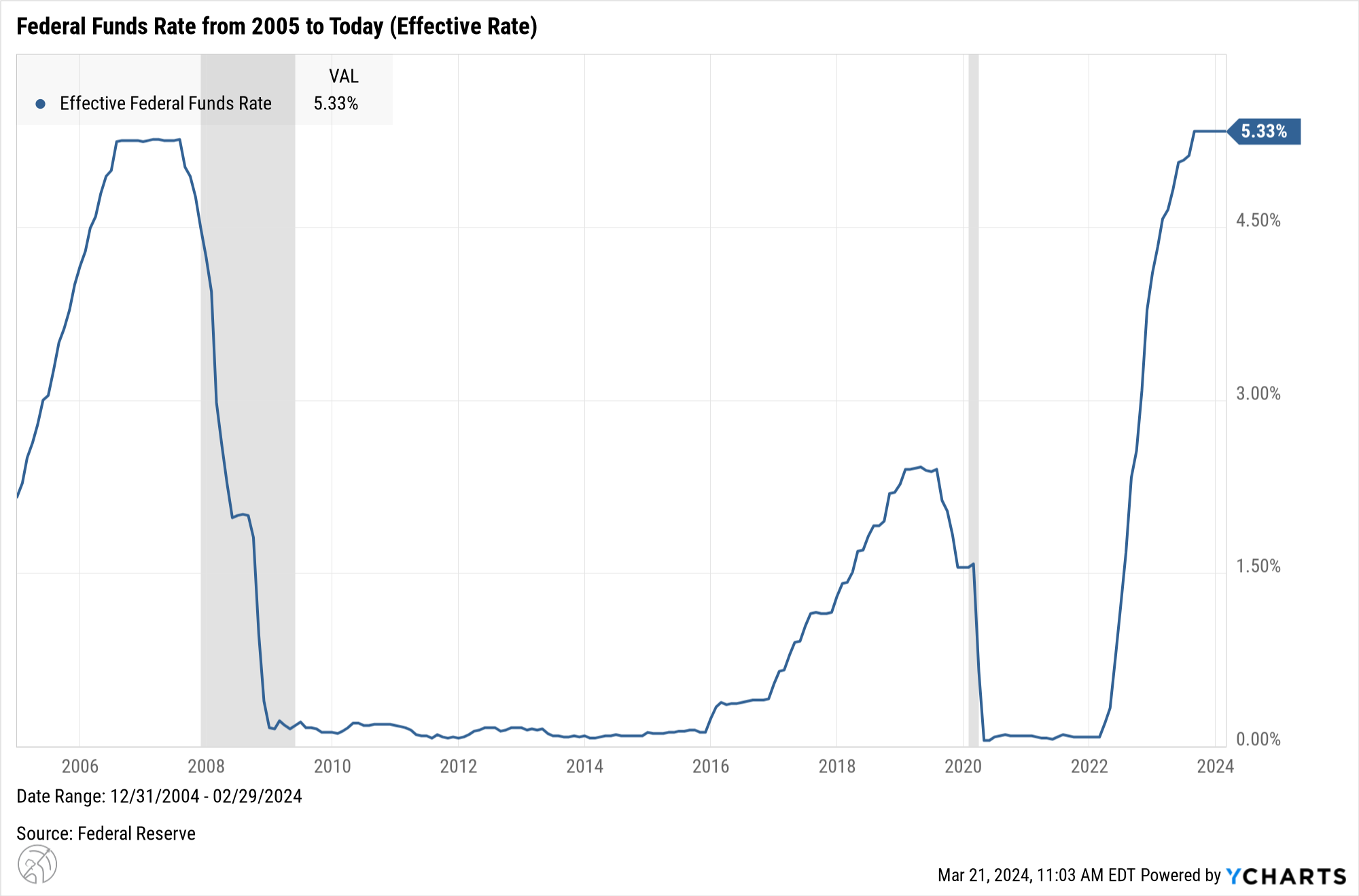

At the start of the pandemic, the federal reserve dropped interest rates to near zero to stimulate the economy. As a response to increasing inflation, the Federal Reserve finally started increasing interest rates in the beginning of 2022.

Since the start of 2022, you can see large increases in the federal funds rate in response to rising inflation. This shift in monetary policy led to an upward trajectory in interest rates across the economy including mortgage rates, credit card rates, and new loan issuances.

The Federal Reserve was slow to begin raising rates, but once they initiated the process, they accelerated at an unprecedented pace, setting a historic precedent for interest rate adjustments.

Higher interest rates can have significant implications for borrowers across various loan types, including credit card debt, mortgages, and auto loans.

Mortgages: Higher interest rates can lead to increased mortgage rates, making homeownership more expensive. Current homeowners with low interest rate mortgages are reluctant to move and lose their low rate which restricts home supply.

Credit card debt: When interest rates rise, credit card companies increase their rates, resulting in higher borrowing costs for consumers. This can make it more challenging to pay off credit card debt and may necessitate a reassessment of spending habits and repayment strategies.

.png)

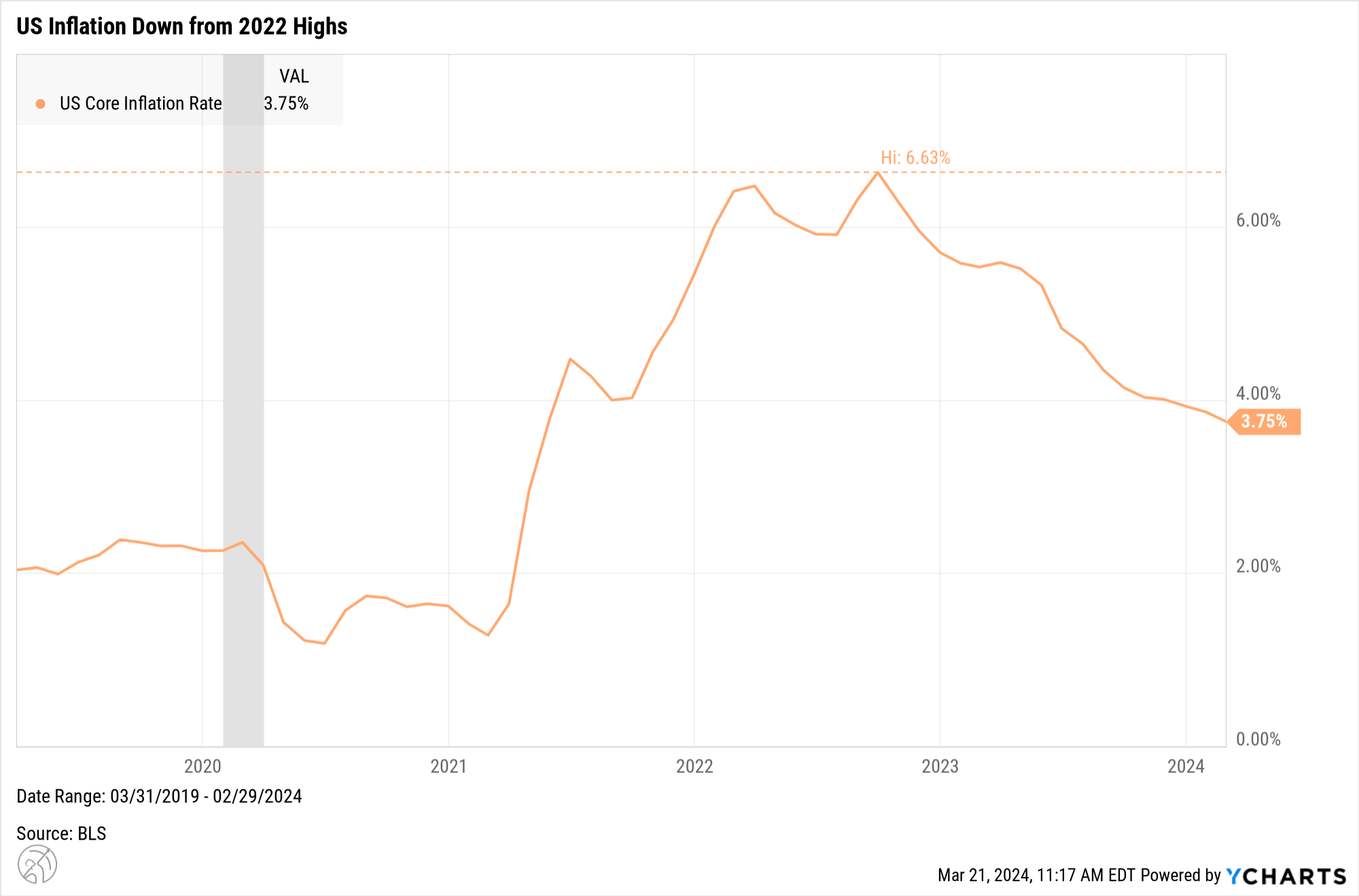

By the autumn of 2023, with inflation on the decline, the Federal Reserve signaled a halt in rate hikes. This pivotal 'pause' significantly contributed to the stock market rally that closed out the year in 2023.

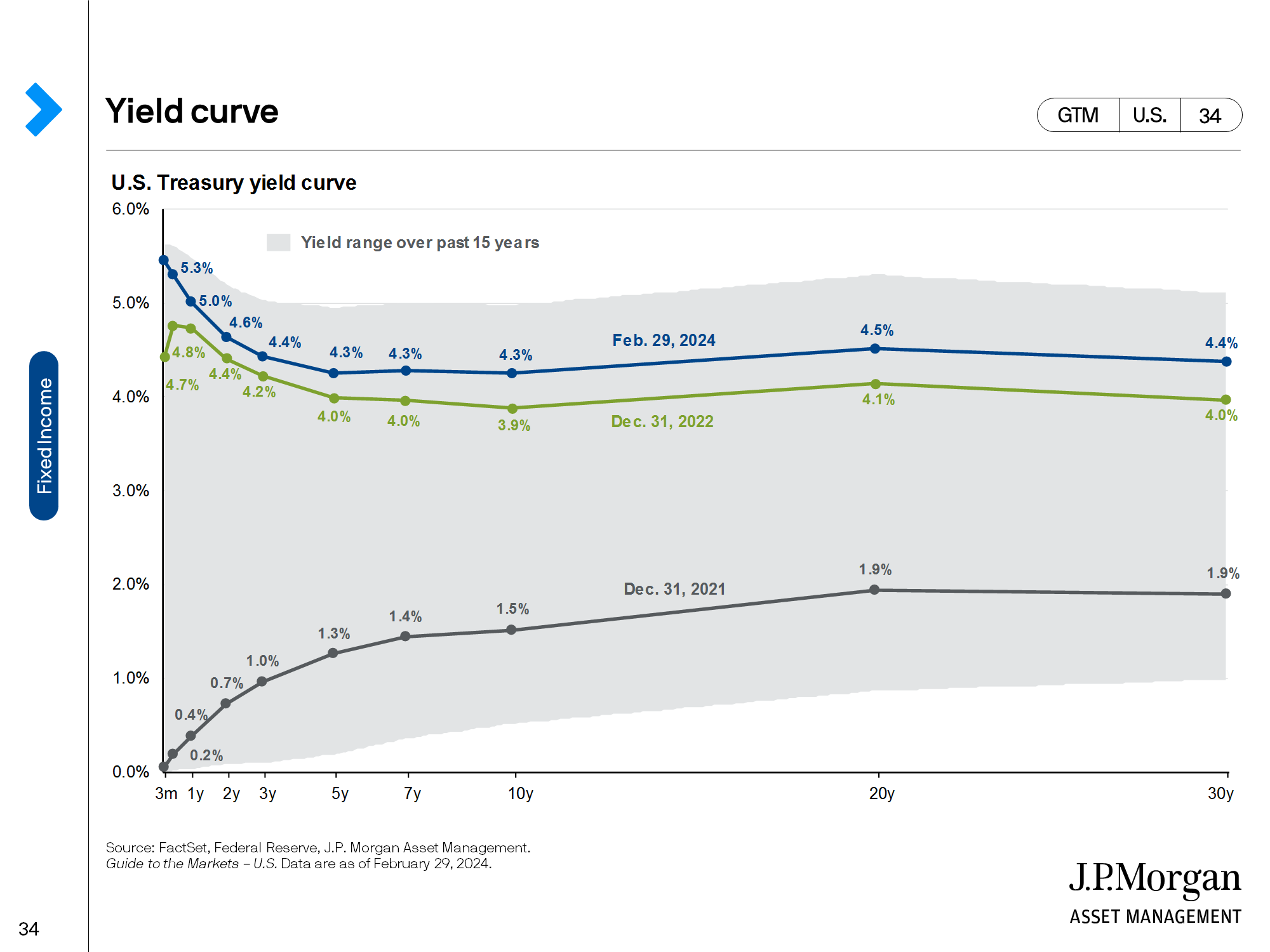

For our clients with excess cash, we've found high quality money market funds earning over 5% in annual interest. These types of earnings on cash were unheard of a few years ago.

On the chart below, you can see the different interest rate yields today (blue line) compared to the end of 2021 (gray line). As you can see, we are now able to earn much more in interest when we buy US Treasuries.

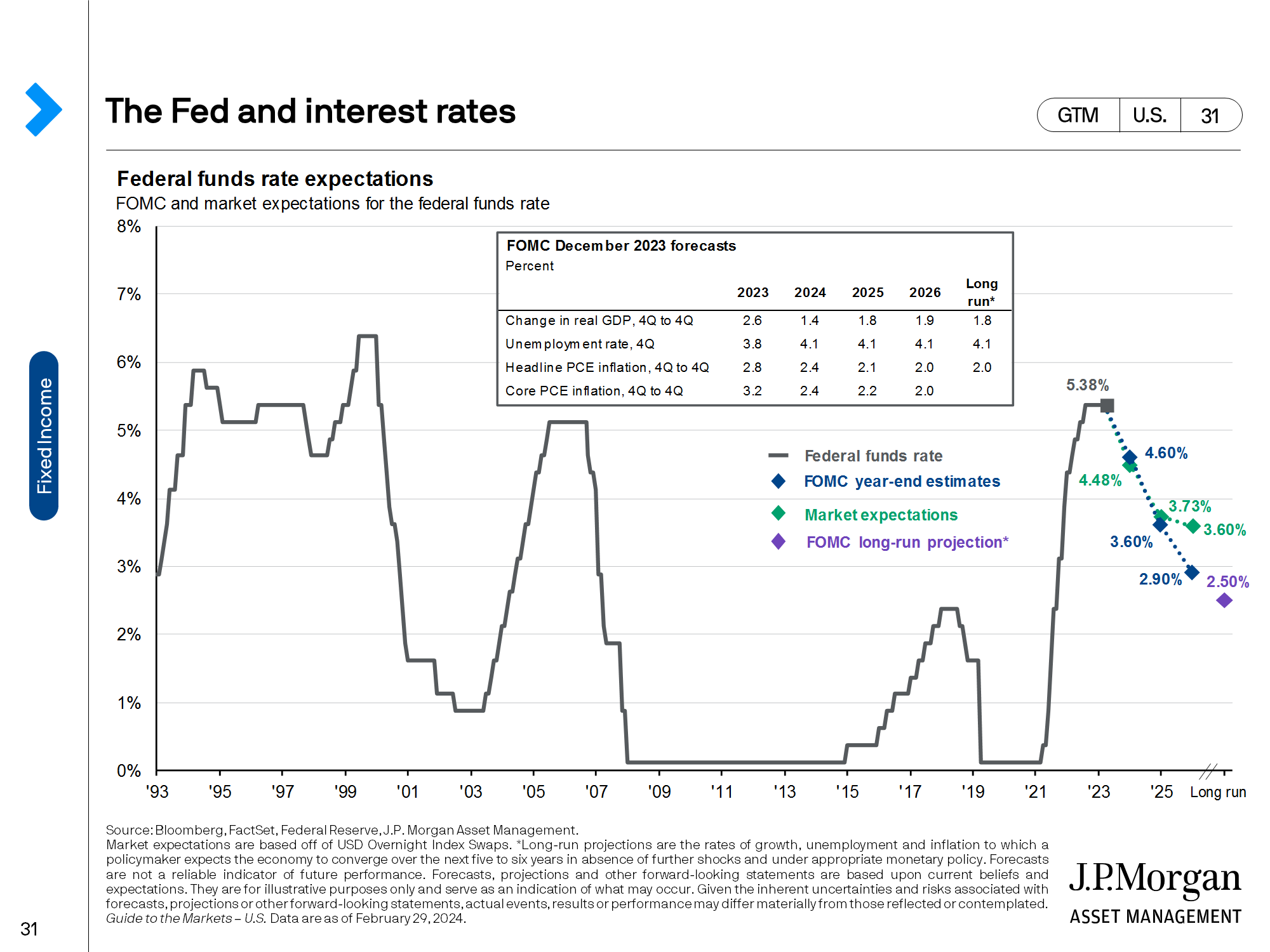

Forecasting interest rates is hard. Period. However, right now the market and Fed are both on the same page for the first time in a while. The biggest risks to the forecast are unforeseen events such as geopolitical shocks, pandemics, etc. that are impossible to predict.

We currently expect three rate cuts during 2024 starting in June. If you look at the green and blue line on the right side of the chart, you can see the reduction in rates over the next few years.

The rate cuts will likely have their biggest impact on money market interest rates. As soon as the Fed begins cutting rates, we expect the 5% interest rates in the money market funds to decline quickly.

Strategies to consider carefully and evaluate before making any changes:

Locking in higher rates through buying individual bonds or bond funds with targeted maturities.

Shifting money market fund assets to other income producing investments in CDs, Bonds, or Private Credit.

Waiting to purchase a home or refinance until rates decline.

Paying off high interest rate credit card debt to avoid 20% interest charges.

One our preferred approaches to locking in longer term interest rates is adding bond ladders to client portfolios through the use of iShares iBonds ETFs. The ETFs provide diversified exposure to bonds, set maturity dates, monthly distributions, and ease of trading. For example, an investor could potentially lock in 5 - 7% in interest income by purchasing bond funds targeted to mature over the next few years. Investors should evaluate risks and exposures carefully before investing.

Staying informed about the evolving narrative of interest rates in the coming months is crucial for investors to make well-informed decisions.

Helpful Articles on Interest Rates from the Wall Street Journal.

4 Ways to Lock In Yields Above 5%

The Fed’s Conundrum: Interest Rates Are Both Too High—and Too Low

Fed Officials Still See Three Interest-Rate Cuts This Year, Buoying Stocks

Disclosure

The views, opinions, and content presented herein are for informational purposes only. They are not intended to reflect a current or past recommendation; investment, legal, tax, or accounting advice of any kind; or a solicitation of an offer to buy or sell any securities or investment services. The advisor does not provide legal advice. Nothing presented should be considered to be an offer to provide any product or service in any jurisdiction that would be unlawful under the securities laws of that jurisdiction. The charts and/or graphs contained herein are for educational purposes only and should not be used to predict security prices or market levels. Before taking any action, you should first consult with a tax, legal, or financial professional.